The Polytechnique decision is a warning shot. It exposed the legal fault line where the US Cloud Act collides with GDPR, making traditional cloud contracts a liability minefield for European institutions. This isn’t a theoretical debate anymore, it’s an operational crisis that’s accelerating a $80 billion sovereign cloud boom.

You need to understand where your data really goes and who controls it when regulators, or attackers, come knocking. Keep reading to see why the old rules no longer apply and what you must do next.

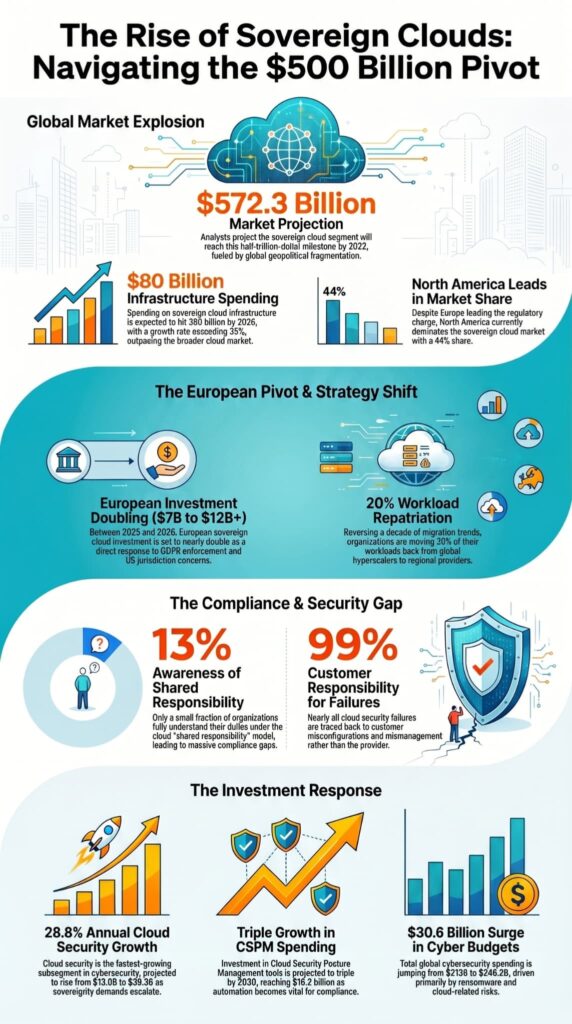

Key Statistics on the EU Cloud Sovereignty Crisis

The collision of data privacy laws and national security mandates is reshaping the global cloud landscape. Spending, security priorities, and infrastructure strategies are all pivoting in response to the legal risks highlighted by cases like École Polytechnique’s suspension of Microsoft 365. The numbers tell a story of rapid, regulation-driven change.

- $80 billion / 35%+ growth – Sovereign cloud infrastructure spending is expected to hit this mark by 2026, growing faster than the broader cloud market as governments and enterprises seek localized control.

- $7B → $12B+ (2025-2026) – European sovereign cloud investment is nearly doubling in a single year, a direct response to GDPR enforcement and fears over US jurisdiction.

- $572.3 billion by 2032 – Analysts project the sovereign cloud market will become a half-trillion-dollar segment, fueled by global geopolitical fragmentation.

- 44% market share – North America currently dominates the sovereign cloud market, even as Europe leads the regulatory charge, highlighting a complex global dynamic.

- 20% workload repatriation – Organizations are actively moving a significant portion of workloads back from global hyperscalers to regional providers, reversing a decade of cloud migration trends.

- 13% awareness – A shockingly low number of organizations fully understand their responsibilities under the cloud “shared responsibility” model, creating massive security and compliance gaps.

- 99% customer responsibility – Nearly all cloud security failures are traced to customer misconfigurations and mismanagement, placing the operational burden squarely on the user.

- $4.7B → $6.3B → $16.2B CSPM spending – Investment in Cloud Security Posture Management tools is soaring, with spending projected to triple by 2030 as automation becomes critical for compliance.

- $213B → $246.2B cybersecurity spending – Global cybersecurity budgets are surging, with a $30.6 billion single-year increase, driven by ransomware and cloud-related risks.

- $13.0B → $17.1B → $39.3B cloud security growth – The cloud security subsegment is the fastest-growing area in cybersecurity, expanding at 28.8% annually due to escalating compliance and sovereignty demands.

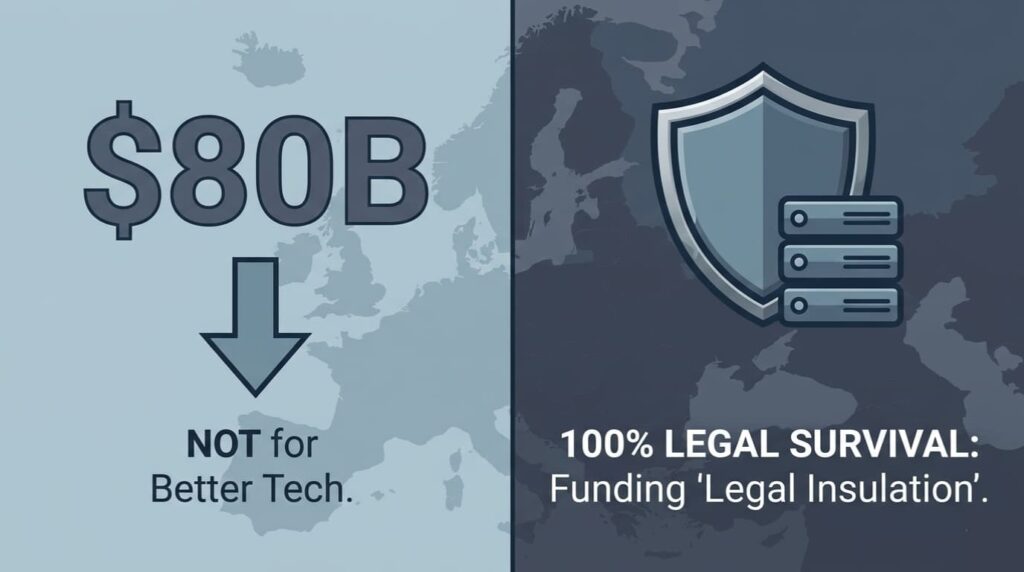

$80 Billion in Sovereign Cloud Spending by 2026 Signals a Regulatory Earthquake

According to Gartner, that staggering $80 billion sovereign cloud spending figure isn’t about better technology. It’s about legal survival. Governments and regulated industries, spooked by the Polytechnique case, are now funding their own legal insulation. They’re buying infrastructure where data never leaves a defined legal jurisdiction, because the alternative is constant anxiety over which government’s warrant arrives first.

The US Cloud Act and GDPR aren’t just incompatible in theory. They create impossible choices in practice. This spending boom is the market pricing in that risk.

For MSSPs, this creates an urgent consulting need. Every euro moving to a sovereign cloud requires a vendor-agnostic audit to answer one question: does this setup actually comply, or are we just moving the problem to a different data center?

| Primary Driver | Impact on Sovereign Cloud Adoption | MSSP Audit Implication |

| GDPR Enforcement | Forces explicit data localization and transfer controls. | Requires mapping all data flows and access points against Article 44-50. |

| US Cloud Act Concerns | Creates fear of foreign law enforcement access to EU data. | Demands legal review of provider jurisdiction and data center ownership. |

| Public Sector Procurement | Mandates preference for EU-based providers (e.g., GAIA-X). | Necessitates compliance validation against specific national procurement frameworks. |

Europe’s Sovereign Cloud Market Doubling to Over $12B Is a Direct Reaction

According to IDC and European sovereign cloud market forecasts, the jump from $7B to over $12B in European sovereign cloud spending in one year isn’t an organic trend. It’s a stampede.

The Polytechnique decision was a catalyst, but the fuel was already there: decades of transatlantic distrust over surveillance finally meeting an enforceable EU law with teeth, GDPR.

France and Germany are leading this charge, not just with words, but with procurement budgets. Their public sectors and critical industries are being steered away from US hyperscalers by policy.

This isn’t about hating Microsoft or Amazon. It’s a cold calculation. When a French university’s emails can be subpoenaed by a US court under the Cloud Act, the entire premise of using that service for EU citizen data collapses. The market is reacting to that broken premise.

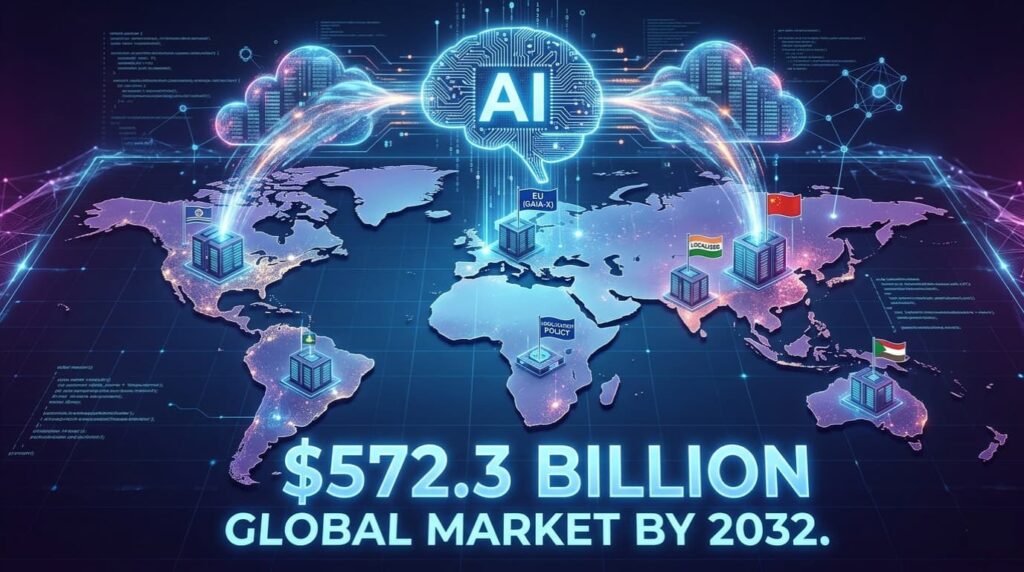

The Path to a $572.3 Billion Global Sovereign Cloud Market by 2032

According to MarkNtel Advisors, the projection of a $572.3 billion sovereign cloud market seems audacious until you look at the underlying forces.

It’s not just Europe. Every major region is crafting its own data sovereignty rules. China has its own cloud ecosystem. India has data localization policies. AI and machine learning workloads are generating unprecedented volumes of sensitive data, making sovereignty a first-order concern across healthcare, finance, government, and critical infrastructure.

The cloud is fragmenting along geopolitical lines. This long-term growth means the tools and expertise for managing compliance across fragmented environments will become incredibly valuable.

MSSPs that build practices around sovereignty auditing and multi-cloud governance are positioning themselves for a decade-long market wave.

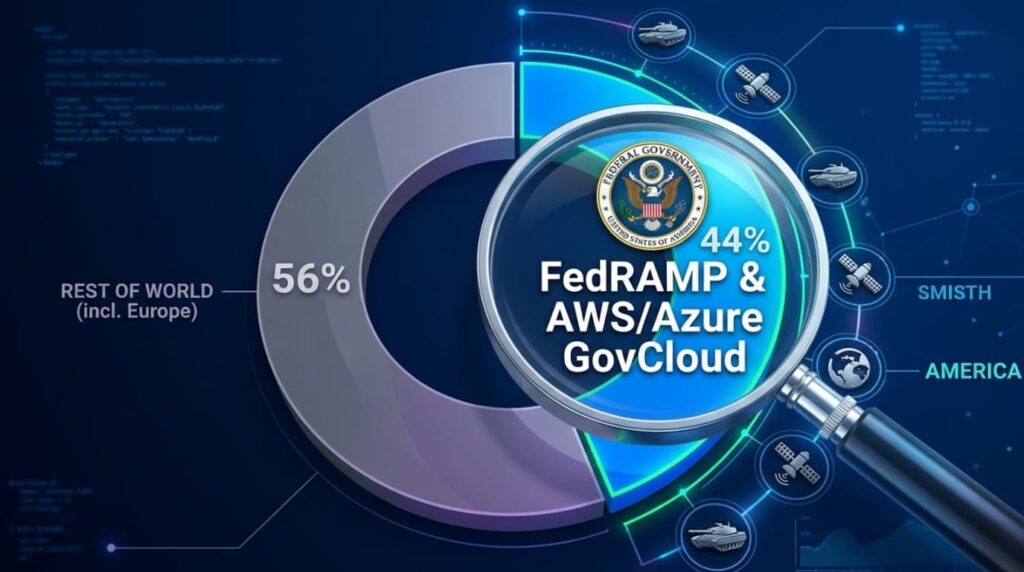

Why North America Holds 44% of the Sovereign Cloud Market

According to Fortune Business Insights, North America currently holds 44% of the sovereign cloud market despite Europe leading the regulatory narrative.

The irony is obvious. While Europe worries about US laws, the United States itself is the biggest spender on sovereign cloud infrastructure. That market share is driven heavily by the US federal government and defense contractors.

Programs like FedRAMP and sovereign environments such as AWS GovCloud and Azure Government exist for the same reason Europe is pursuing sovereignty: control over sensitive data. It proves a larger point. Sovereignty is no longer a regional issue. It’s a universal response to geopolitical distrust.

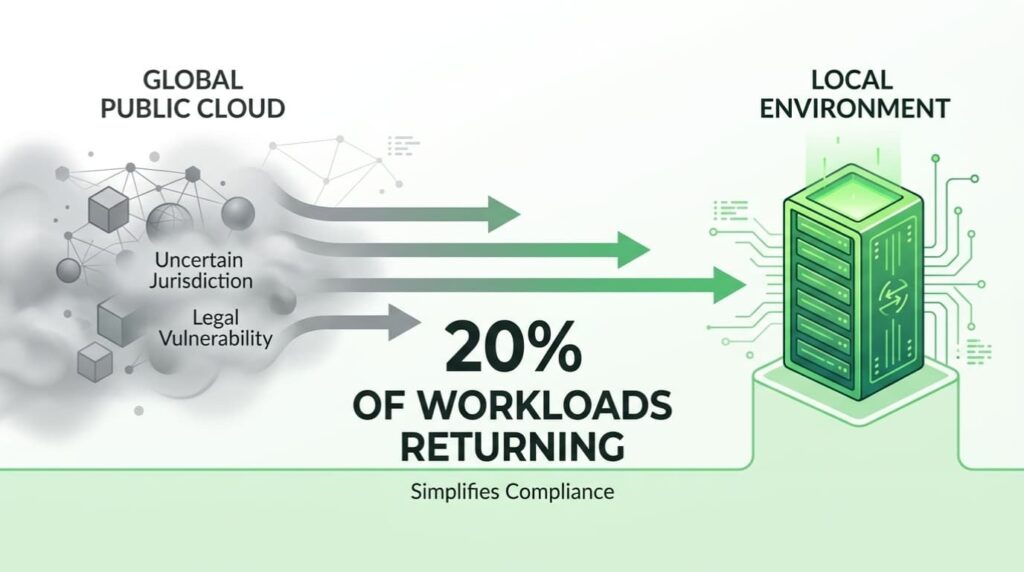

20% of Cloud Workloads Are Coming Back Home

According to Citrix enterprise cloud research, workload repatriation is accelerating as organizations move workloads back from hyperscalers to local providers and private environments. That 20% figure represents a costly and complex reversal of the cloud-first era.

Latency and cost predictability matter, but legal control is becoming the dominant driver. In a global public cloud, organizations often cannot confidently answer where data physically resides at all times. Under GDPR, that uncertainty is a compliance risk.

Under the US Cloud Act, it becomes a legal vulnerability. Bringing workloads back into a known local jurisdiction simplifies the compliance equation dramatically.

Only 13% of Organizations Grasp Shared Responsibility

According to research published by Taylor & Francis Online, only 13% of organizations fully understand the cloud shared responsibility model.

That statistic is alarming because most organizations still assume the cloud provider handles “security.” In reality, providers secure the infrastructure. Customers remain responsible for configurations, access keys, permissions, encryption settings, and governance controls inside the cloud environment.

This knowledge gap is where breaches happen. It also sits at the heart of the Polytechnique dispute. The concern wasn’t only Microsoft’s security. It was the inability to fully understand how US laws could apply to data stored inside Microsoft-controlled infrastructure.

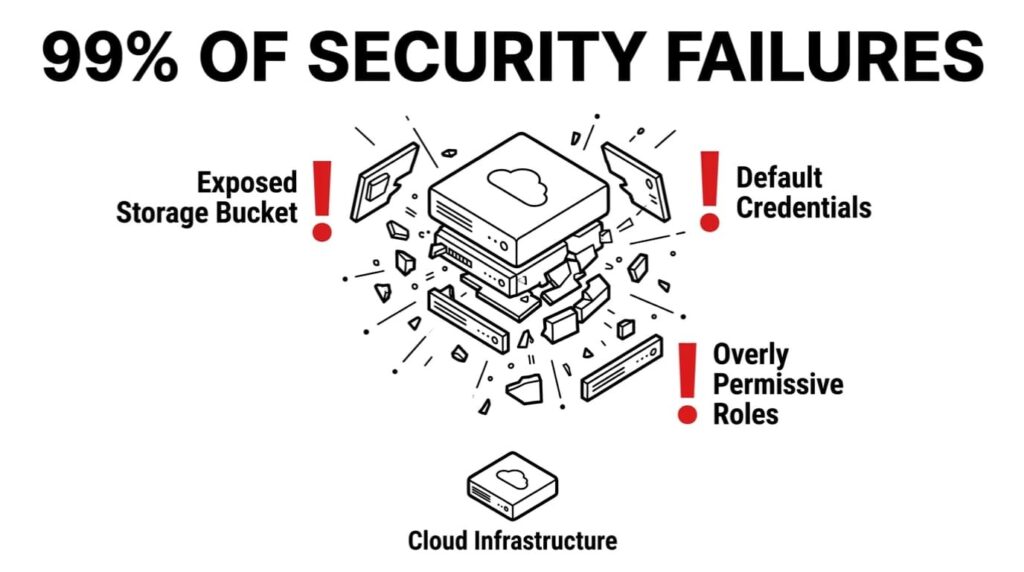

99% of Cloud Security Failures Are Still Your Fault

According to HALOCK cybersecurity research cited in academic studies, 99% of cloud security failures are caused by customer misconfigurations, weak identity management, and poor governance practices.

The hyperscalers’ infrastructure is often highly resilient. Customer environments layered on top of it frequently are not. An exposed storage bucket, default admin credentials, or overly permissive access roles remain some of the most common causes of breaches.

This is why the shared responsibility model increasingly feels structurally imbalanced. Organizations carry most of the operational risk, while providers can still introduce legal exposure through jurisdictional obligations like the US Cloud Act.

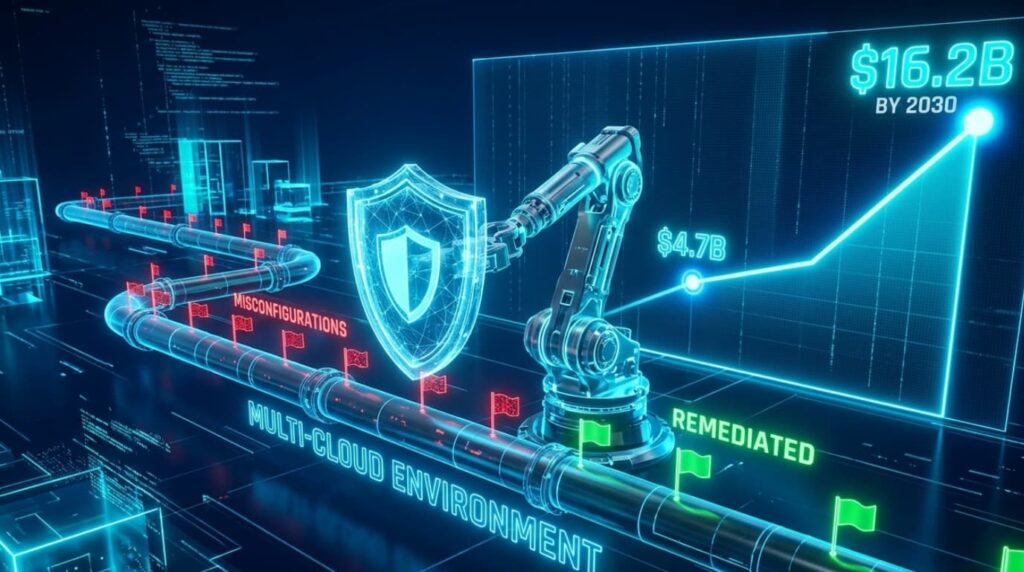

CSPM Spending Tripling to $16.2B Is an Automation Mandate

According to Gartner forecasts, Cloud Security Posture Management spending is projected to surge from $4.7B to $16.2B by 2030.

Organizations cannot manually monitor thousands of cloud resources across sprawling multi-cloud environments anymore.

CSPM platforms automate compliance checks, detect misconfigurations, and continuously enforce governance policies. In sovereignty-focused environments, they also operationalize legal requirements.

For example, organizations can define automated policies preventing sensitive workloads from being deployed outside approved EU regions.

This transforms sovereignty from a legal aspiration into an enforceable technical control.

Global Cybersecurity Spending’s $30.6B Single-Year Jump

According to Gartner, global cybersecurity spending is increasing from $213B to $246.2B in a single year.

That surge is not only about ransomware or cybercrime. It reflects the convergence of technical attack risks with escalating legal and regulatory exposure.

A breach is already expensive. A breach involving improperly stored EU citizen data can trigger GDPR investigations, compliance violations, litigation, and reputational damage simultaneously.

Boards are increasingly funding cybersecurity as a legal resilience strategy rather than simply an IT function.

Cloud Security’s 28.8% Growth Makes It the Top Priority

According to Gartner, cloud security is expanding at 28.8% annually, making it the fastest-growing segment in cybersecurity.

The attack surface has fundamentally shifted. Data now lives across SaaS platforms, IaaS workloads, APIs, and multi-cloud architectures. Traditional perimeter security models no longer provide adequate visibility or control.

Technologies such as CSPM, Cloud Workload Protection Platforms (CWPP), and SaaS Security Posture Management (SSPM) are becoming foundational requirements for organizations trying to satisfy sovereignty and compliance obligations.

FAQ

What are the biggest security risks during cloud migration?

Cloud Migration projects can expose businesses to security risks such as data breach incidents, insider threat activity, and data exfiltration. Weak security controls, poor network segmentation, and misconfigured cloud infrastructure often increase cyber threats.

Companies should perform a detailed risk assessment, secure encryption keys properly, and strengthen Identity and Access Management before moving systems into a cloud environment.

How does encryption protect cloud environments?

Data Encryption protects sensitive information during Cloud Migration and daily cloud computing operations. Businesses use SSL encryption, encryption at rest, and Bring Your Own Key strategies to secure customer data and internal systems.

Hardware Security Modules also protect encryption keys from unauthorized access. Strong encryption reduces data loss prevention failures across public cloud, private cloud architecture, and hybrid architecture environments.

Why is identity management important in cloud security?

Identity access management helps organizations control who can access applications, cloud infrastructure, and sensitive data centers.

Role-based access control, digital identities, and two-factor authentication reduce unauthorized access risks during SAP cloud migration and application modernization projects.

Strong Cloud Migration Security practices also support compliance requirements, data sovereignty policies, and secure remote work access across multi-cloud architectures.

Which security tools help secure cloud migration projects?

Businesses use Cloud Security Posture Management platforms, Threat Detection systems, Security Information and Event Management tools, and Vulnerability Management solutions to strengthen cloud security.

Web Application Firewalls, Next-Generation Firewalls, API security controls, and Application Security Testing also identify weaknesses before deployment.

These security features improve Cyber resilience and protect cloud providers, cloud service providers, and public cloud environments from attacks.

How can companies avoid compliance problems during cloud migration?

Organizations should review compliance requirements, security standards, and data protection regulations before starting Cloud Migration projects. Many businesses follow the Cloud Security Technical Reference Architecture and Federal Risk and Authorization Management Program guidelines to improve security strategy planning.

Regular audits, business continuity management testing, and Zero Trust Protection policies also reduce vendor lock-in risks and long-term security gaps.

Building a Resilient Cloud Strategy for a Fragmented Future

EU cloud sovereignty is no longer a theoretical concern. Organizations now need clear visibility into where data lives, who can access it, and how regulatory shifts may impact operations. A resilient strategy starts with auditing cloud exposure, reducing critical dependencies, and building governance that can adapt as regulations evolve.

At MSSP Security, the focus is on helping businesses strengthen cloud governance, improve security visibility, and prepare for the growing realities of data sovereignty in a changing global landscape.